In today's world, if you are residing in another part of the world, learning how to manage finances becomes crucial. Whether you're an individual receiving funds from family overseas or a business engaged in cross border transactions, not knowing TDS on foreign remittances can make you fall into legal trouble due to not following compliance standards, such as FEMA compliance.

In this comprehensive guide, we will explore every important aspect of TDS implications for foreign remittances. From understanding the TDS rates to navigating recent regulatory changes, we will cover everything you need to know to help you make informed financial decisions. Whether you're an individual sending money abroad or a business handling international transactions, understanding the tax on foreign remittance in India is crucial.

So, let us take a closer look at what TDS means for foreign remittances and how it applies to you in the next section.

Understanding TDS on Foreign Remittances

What is TDS?

TDS (Tax Deducted at Source) refers to taxes that are deducted at the source of income before the amount is credited to the recipient.

How Does It Apply to Foreign Remittances?

When sending or receiving funds internationally, banks or remittance service providers deduct TDS before the money is transferred. The deducted tax is then deposited to the Indian government.

How TDS Affects Your Foreign Remittance Transactions

Impact on Transaction Amount

TDS directly affects the amount you receive or send. When applicable, a portion of the remitted amount is deducted at the source, reducing the final sum transferred.

Compliance Requirements

Foreign remittances are now subject to additional compliance requirements. If you require guidance on complex registration processes such as GST registration in Gurgaon, then reach out to the top GST consultant in Gurgaon. The compliance requirements of foreign remittances are:

- Form 15CA/15CB: Required for most taxable foreign remittances.

- PAN Card: Essential for TDS deduction and reporting.

- Documentation: Maintain records of all transactions and TDS deductions.

Read More: A Guide: Form 15CA and 15CB for Cross-Border Payments

How to calculate TDS on foreign remittances

Calculating TDS on foreign remittances involves a simple process:

- Determine the remittance amount in Indian Rupees

- Identify the applicable TDS rate

- Multiply the remittance amount by the TDS rate

- Deduct the calculated TDS from the remittance amount

For example, if you're sending ₹1,00,000 for education purposes:

- TDS rate: 5%

- TDS amount: ₹1,00,000 × 5% = ₹5,000

- Net remittance: ₹1,00,000 - ₹5,000 = ₹95,000

Currency conversion considerations

When dealing with foreign remittances, currency conversion plays a crucial role in TDS calculations. Consider the following:

- Use the exchange rate on the day of remittance

- Refer to RBI reference rates for accurate conversions

- Factor in any bank charges or fees in your calculations

Remember, accurate currency conversion is essential for proper TDS compliance and reporting. Now that we've covered TDS rates and calculations, let's explore some recent changes in TDS regulations for foreign remittances.

Recent Changes in TDS Regulations for Foreign Remittances

New TDS Threshold for Foreign Remittances

One of the most significant changes in TDS regulations for foreign remittances is the introduction of a new threshold. As of July 1, 2023, TDS applies only when foreign remittances exceed ₹7 lakh per financial year under the Liberalized Remittance Scheme (LRS).

✔️ Transactions below ₹7 lakh in a financial year are exempt from TDS (except for investments & other high-tax categories).

✔️ For amounts exceeding ₹7 lakh, TDS is applicable at different rates based on the nature of the remittance.

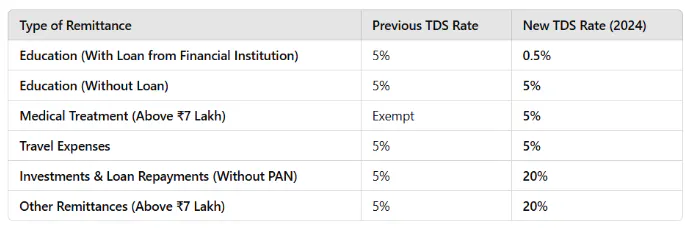

Updated TDS Rates (2024 Latest Data)

The government has also revised TDS rates for various foreign remittances, making taxation more structured and differentiated based on the purpose of the transfer.

Key Clarifications on TDS Rates

✅ Education Expenses (With Loan): If remittance is for education expenses via a financial institution loan, TDS is reduced to 0.5%.

✅ Medical Remittances: Now subject to 5% TDS if above ₹7 lakh (earlier fully exempt).

✅ Investments & Loan Repayments: If PAN is not provided, TDS is 20%.

✅ General Foreign Remittances (Above ₹7 lakh): Now taxed at 20%, a significant increase from 5% previously.

Exemptions and Relaxations

To ease the burden on specific groups, the government has introduced certain exemptions and relaxations:

✔️ Remittances for education loans taken from registered financial institutions now attract only 0.5% TDS instead of 5%.

✔️ Senior Citizens (Aged 60 and above): Higher exemption threshold of ₹10 lakh per financial year for foreign remittances.

✔️ Medical Remittances: TDS exemption applies only under specific conditions (like payments directly to a hospital or medical provider).

Updated Reporting Requirements for Foreign Remittances

With the stricter tax compliance framework, the government has tightened reporting requirements for foreign remittances:

📌 Banks & Financial Institutions must

- Report all foreign remittances in their quarterly TDS returns (Form 26Q).

- Verify PAN details for transactions above ₹2.5 lakh before processing remittances.

- Ensure correct TDS deduction before transferring funds.

📌 Individuals must

- Declare foreign remittances in their annual Income Tax Returns (ITR).

- Submit Form 15CA (for taxable remittances) before transferring funds abroad.

- Obtain Form 15CB (certified by a Chartered Accountant) if remittance exceeds ₹5 lakh and is taxable.

New Compliance Rules for Form 15CA & 15CB

How to Reduce TDS Using DTAA (Double Taxation Avoidance Agreement)

DTAA allows individuals and businesses to reduce TDS liability on international transactions. This prevents individuals from having to pay taxes twice both countries.

To Avail DTAA Benefits:

- Submit Tax Residency Certificate (TRC) from the foreign country.

- Provide Form 10F to the deductor.

- Mention DTAA in Form 15CA/15CB.

How to Claim a TDS Refund on Foreign Remittances

If TDS was deducted at a higher rate, you can claim a refund through the Income Tax Return (ITR) filing process.

Step-by-Step Process to Get a TDS Refund:

- Download Form 16A (TDS certificate) from the deductor.

- File your ITR, mentioning the TDS paid.

- Claim credit for TDS in the appropriate section.

- Attach DTAA documents (TRC, Form 10F) if applicable.

- Track your refund status via the Income Tax portal.

✅ Refunds are usually processed within 3-6 months.

Common Mistakes to Avoid in Foreign Remittance TDS

1. Overlooking TDS Applicability

One of the most common mistakes individuals and businesses make is assuming that TDS does not apply to their foreign remittances.

2. Ignoring DTAA Benefits

Failing to utilize Double Taxation Avoidance Agreement (DTAA) benefits can lead to higher TDS deductions on foreign remittances. DTAA allows individuals and businesses to claim reduced TDS rates or tax credits, minimizing unnecessary tax outflows.

3. Incorrect TDS Rate Application

Applying the wrong TDS rate can lead to unnecessary tax deductions, penalties, or legal scrutiny.

4. Failing to Obtain Necessary Documentation

Proper documentation is critical for TDS compliance and avoiding legal complications. However, many individuals and businesses fail to maintain the required paperwork, leading to potential penalties.

5. Not Keeping Transaction Records

Maintaining detailed transaction records is essential for audit compliance, tax filing, and TDS verification. Missing records can lead to disallowance of expenses, difficulty in claiming tax refunds, or penalties during tax assessments.

6. Missing TDS Deposit Deadlines

TDS deducted on foreign remittances must be deposited with the Income Tax Department within specific deadlines. Failing to deposit TDS on time can result in penalties, interest charges, and legal consequences.

Read Also: The Ultimate Guide To Taxation Of Expatriates In India

Conclusion

When it comes to cross border transactions, it is important to take note of TDS deductions to save expenses. This allows you to save yourself from unexpected taxations when you are receiving funds from someone abroad. Ensure financial health by keeping yourself aware about TDS rates!